AI's HBM buildout shows up on entry-phone BOMs and Transsion's P&L

Hyperscaler HBM demand and budget-phone memory draw from the same wafer pool, and Transsion's profit warning is the first downstream bill.

AI’s HBM buildout shows up on entry-phone BOMs and Transsion’s P&L

TL;DR

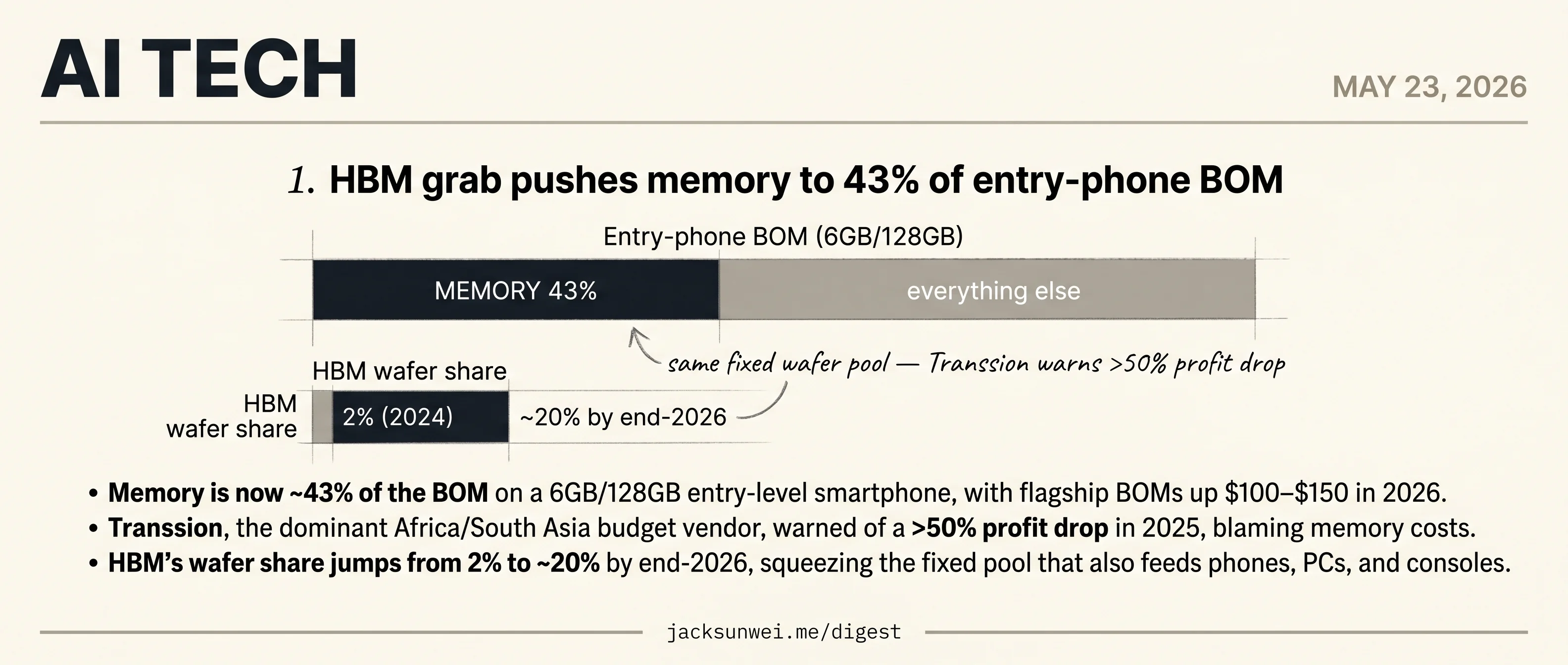

- Memory hits 43% of a 6GB/128GB entry-phone BOM, with flagship BOMs up $100–150 in 2026.

- Transsion warns of a >50% profit drop in 2025, citing memory costs.

- HBM jumps from 2% to ~20% of wafer share by end-2026, squeezing phones, PCs, and consoles.

- Morgan Stanley models HBM overshooting demand 66% in 2027 if hyperscaler growth normalizes.

The AI infrastructure buildout has a bill, and today’s tech read is about who’s paying it first. HBM and commodity DRAM/NAND draw from the same finite wafer pool, so when hyperscaler HBM allocations jump from 2% to ~20% of wafer share inside a year, the squeeze lands on every other device that needs memory — phones, PCs, consoles. The clearest tell isn’t a flagship price hike; it’s Transsion, the budget-phone vendor that dominates Africa and South Asia, warning of a >50% profit drop in 2025 with memory costs named as the cause. Memory is now roughly 43% of the BOM on an entry-level 6GB/128GB handset — a structural shift, not a cyclical bump. The bear case, per Morgan Stanley, is HBM overshooting demand 66% by 2027 if hyperscaler growth normalizes. Until then, the AI capex story has a downstream cost line, and it’s already showing up outside the AI industry’s own P&Ls.

HBM grab pushes memory to 43% of entry-phone BOM

Source: simon-willison · published 2026-05-22

TL;DR

- Memory is now ~43% of the BOM on a 6GB/128GB entry-level smartphone, with flagship BOMs up $100–$150 in 2026.

- Transsion, the dominant Africa/South Asia budget vendor, warned of a >50% profit drop in 2025, blaming memory costs.

- HBM’s wafer share jumps from 2% to ~20% by end-2026, squeezing the fixed pool that also feeds phones, PCs, and consoles.

- Morgan Stanley sees HBM overshooting demand by 66% in 2027 if hyperscaler growth normalizes — the bear case on the squeeze.

The mechanism

There are three memory makers left, their wafer capacity is fixed in the short run, and HBM is now eating it. David Oks’s piece — which Simon Willison flagged this week — lays out the arithmetic: HBM allocation is rising from 2% of wafers to roughly 20% by end-2026, and a gigabyte of HBM consumes more than three times the wafer area of a gigabyte of DDR or LPDDR. Every HBM stack Nvidia buys is silicon that doesn’t become smartphone RAM.

The “three remaining manufacturers” framing matters because of how they behave. Post-Qimonda and post-Elpida, the survivors adopted what TechInvestments.io calls explicit “capital discipline” — analysts describe it as tacit collusion, with supply cuts signaled on earnings calls to keep rivals from expanding 1. That’s why this shortage looks structurally different from the 2017 cycle: under-provisioning is the strategy, not the accident.

The damage is already booked

Counterpoint’s numbers are the receipts. Memory is now ~43% of the BOM on a 6GB/128GB entry-level phone; mid-range memory share has risen from 14% to 20%; flagship BOMs are up $100–$150 in 2026 2. Those aren’t projections — they’re current quarter.

The first corporate casualty is exactly the company Oks’s thesis predicts. Transsion — the Tecno/Infinix/itel parent that dominates sub-$100 phones across Africa and South Asia — warned of a >50% net profit collapse in 2025, citing component costs 3. If you wanted a single data point to validate “AI is killing the cheap smartphone,” that’s it.

It’s not just phones

NAND shares fab footprint with DRAM, so the spillover is broad: 1TB SSD prices have more than doubled since 2024, and memory now accounts for ~20% of PS5 manufacturing cost — squeezing console subsidies and, eventually, game pricing 4. The horizontal read is that every memory-bearing device is repricing, not just the budget handset Oks foregrounds.

Two things that could break the story

China. CXMT has gone from 100K to 300K wafer-starts per month and is now the global LPDDR4X leader — precisely the chemistry inside the “dying” budget phone. Corsair has reportedly begun shipping CXMT DRAM in mainstream PC products, a notable Western-brand capitulation 5. The sub-$100 phone may not die so much as relocate its bill of materials to Hefei, at a 3–4 year node lag.

Hyperscaler digestion. Morgan Stanley-aligned analysis argues 2026 is peak “scale-out shock,” after which HBM could overshoot demand by up to 66% in 2027 as Samsung, SK Hynix, and Micron capex finally lands 6. If AI capex decelerates from triple-digit to 15–30% growth — or if memory-compression techniques reduce per-cluster RAM — the discipline cracks and the supercycle inverts inside 18 months.

What’s actually at stake

The interesting variable isn’t whether HBM stays tight — it’s whether the Big Three’s discipline survives a single defector. CXMT grabbing share, or Samsung deciding it wants Nvidia’s wallet more than it wants the cartel, would unwind the squeeze quickly. Until then, the cheap smartphone is a casualty of an accounting choice made in three boardrooms, not a technology limit.

Footnotes

-

TechInvestments.io — https://www.techinvestments.io/p/history-and-outlook-of-the-memory

↩Post-2012, the ‘Big Three’ survivors moved toward ‘capital discipline’… deliberately limiting capex and production capacity to keep prices stable. Experts describe this as ‘tacit collusion’ where companies signal supply cuts through public earnings calls to discourage rivals from expanding.

-

Counterpoint Research — https://counterpointresearch.com/en/insights/Memory-Price-Surge-Triggers-Shifts-in-Smartphone-BOM-Structure

↩Memory now accounts for roughly 43% of the total BOM for a typical 6GB/128GB entry-level configuration… BOM costs for premium models will rise by $100 to $150 in 2026.

-

TrendForce on Transsion — https://www.trendforce.com/news/2026/01/30/news-chinese-smartphone-maker-transsion-warns-2025-net-profit-could-plunge-50-on-soaring-memory-costs/

↩Transsion Holdings, the leading vendor in Africa, reported a net profit decline of over 50% in 2025, specifically citing soaring component costs.

-

Game Developer — https://www.gamedeveloper.com/business/how-a-surge-in-memory-prices-will-affect-the-games-industry

↩The combined memory in a PlayStation 5 now accounts for roughly 20% of its manufacturing cost, forcing platform holders to reduce hardware discounts; 1TB SSD prices have more than doubled since 2024.

-

↩CXMT is now the leading supplier of LPDDR4X globally… Western PC hardware brands like Corsair have begun integrating CXMT DRAM chips into mainstream products to ensure availability.

-

BingX market analysis (Morgan Stanley view) — https://bingx.com/en/learn/article/roundhill-memory-etf-dram-outlook-and-price-prediction-is-dram-a-good-investment

↩The supply of HBM is projected to outpace demand by up to 66% as early as next year if hyperscale appetites normalize… 2026 represents the ‘scale-out shock’ peak, after which the market will shift from frantic capacity-building to utilization and optimization.